After an accident, the insurance adjuster often seems helpful—even friendly. They say things like "I just want to hear your side of the story" or "We want to get this resolved quickly for you." It sounds reassuring. But make no mistake: the adjuster's job is not to protect you—it's to protect the insurance company's bottom line .

Insurance companies have developed sophisticated playbooks designed to minimize payouts. From delay tactics to lowball offers, recorded statements to surveillance, they employ dozens of strategies to reduce what you receive. The good news? Experienced personal injury attorneys know every trick in that playbook—and they know exactly how to fight back .

The Insurer's Playbook: 10 Tactics Used to Reduce Payouts

Delay & Ignore

Adjusters become non-responsive, offer vague updates, or repeatedly request the same documents. Delays wear you down, hoping you'll abandon the claim or accept less .

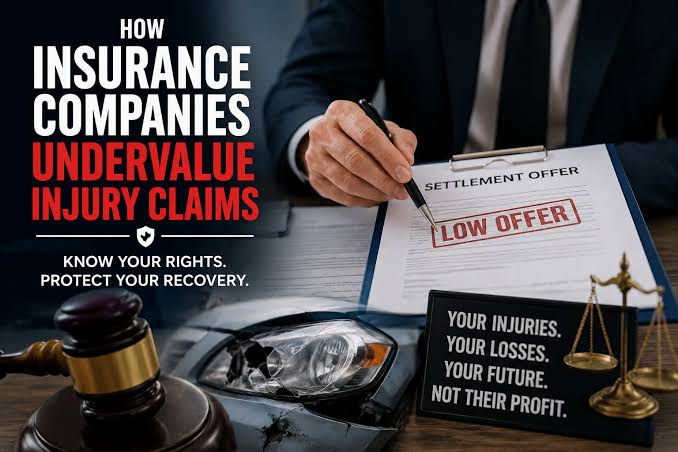

Lowball First Offer

Insurers offer a quick settlement—often within days—hoping you'll accept before understanding your injuries' full extent. These offers rarely cover future medical costs .

Recorded Statements

Adjusters ask for a "quick recorded statement" that sounds routine. But your words can be twisted—even "I'm fine" can be used to argue you weren't seriously injured .

The "Friendly Adjuster"

Adjusters are trained to build rapport and seem sympathetic. This lowers your guard, making you more likely to share information that can be used against you .

Disputing Medical Treatment

Insurers argue your injuries are pre-existing, excessive, or unrelated to the accident. They may send you to a doctor of their choice who downplays your condition .

Surveillance & Social Media

Insurers hire investigators to follow you or scour social media. A photo of you smiling at a family event can be twisted to argue you're not in pain .

Blaming You (Comparative Fault)

Adjusters twist your words or misinterpret evidence to suggest you were partially at fault. In states with comparative fault, even 1% blame can reduce your payout .

Partial Payments Without Explanation

Insurers issue a check for part of your claim without explaining what's covered or why the rest was denied. Many people cash it, unknowingly waiving rights to the remainder .

Delayed IMEs

Insurers schedule independent medical exams weeks or months after your accident. By then, symptoms may have improved, allowing them to argue injuries weren't serious .

Hiding Behind Policy Language

Insurers cherry-pick policy excerpts to deny coverage, hoping you won't read the full document or understand ambiguities that actually favor you .

The Duel: Insurer's Moves vs. Lawyer's Counters

2026 Insurance Reforms: What's Changing?

Major Auto Insurance Overhauls in Canada

Ontario "Optionality"

Starting July 2026, income replacement, caregiver, and non-earner benefits become optional. Drivers may unknowingly opt out, leaving them without coverage .

Effective July 1, 2026Alberta "Care First"

New no-fault system limits ability to sue for health care costs. Set accident benefits paid out, reducing litigation .

Effective Jan 1, 2027Consumer Trap Warning

Brokers warn savings may be as little as $100 even if drivers drop most coverage—a dangerous trade-off .

The Uber Ballot Battle: Capping Attorney Fees & Medical Costs

California's Epic 2026 Showdown

Uber has proposed a ballot initiative that would cap contingency fees (victims keep 75% of settlements) and limit medical damages to 125% of Medicare rates .

"Uber is trying once again to misuse the democratic process and to disclaim legal responsibility—this time, not just towards their drivers but also towards consumers." — Veena Dubal, UC Irvine Law

The Secret Players: Third-Party Litigation Funding

Insurers are battling "third-party litigation funding"—where unknown investors (often foreign) finance lawsuits in exchange for a cut of settlements. The APCIA calls this a hidden "tort tax" of $5,400 per household .

States fighting back: Georgia, Florida, South Carolina now regulate third-party funding. Congress is considering disclosure laws .

The IME Trap: When "Independent" Isn't Independent

Insurers send you to "independent" medical examiners—doctors they hire and pay. Studies show these doctors routinely downplay injuries and find accidents "not the cause" .

Subrogation: Why the Insurer Gets Paid First

Insurer pays your medical bills

You sue the at-fault party

Insurer demands repayment (subrogation)

You keep the rest

The Hidden "Tort Tax"

per household per year—that's what the insurance industry claims lawsuit abuse costs American families in higher premiums and consumer costs .

Consumer attorneys argue this figure is inflated, but the battle over litigation costs continues in 2026.

How an Attorney Levels the Playing Field

Protecting Yourself: Immediate Steps

Knowledge + Representation = Fair Compensation

Insurance companies have spent decades perfecting their tactics. They know that most claimants have never dealt with them before and don't understand the nuances of policy language, valuation, or negotiation .

But you now know their playbook. From delay and deny to friendly adjusters and lowball offers, you can recognize these strategies for what they are: profit-protection, not victim-support . And when you pair that knowledge with experienced legal representation, the balance of power shifts. Attorneys know how to impose deadlines, demand proper valuation, and fight back against every trick insurers use .

In 2026, with major reforms in Ontario, Alberta, and California's Uber battle, the landscape is shifting. But one thing remains constant: represented claimants receive significantly higher settlements than those who go it alone .