The divorce decree is signed. The judge has made it official. You walk out of the courthouse feeling a mixture of relief, exhaustion, and hope for a fresh start. But here's a hard truth that many people discover too late: the decree is not the finish line—it's the starting point for a mountain of critical paperwork .

Nothing in a divorce happens automatically. The court doesn't call your bank, your retirement plan administrator, or the county recorder's office. That responsibility falls entirely on you . And if you miss these steps, the consequences can be severe: retirement accounts lost, property disputes, credit damage, and even your ex-spouse inheriting your estate .

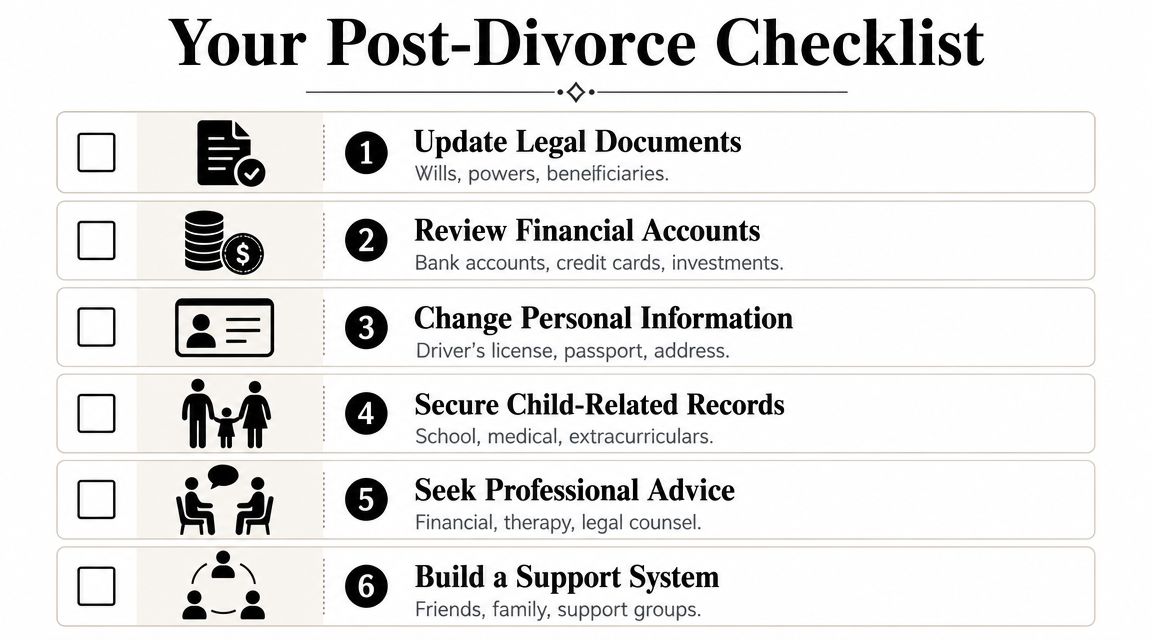

This comprehensive post-divorce checklist covers the critical tasks most people forget—from the 90-day window for retirement transfers to the hidden trap of joint credit cards. Use it to protect your fresh start and ensure your divorce decree becomes reality.

THE CRITICAL WINDOW

Many financial tasks—especially retirement account transfers—must be completed within a narrow window to avoid tax penalties and legal complications .

Step 1: Secure Certified Copies and Update Identification

Order Certified Copies

Secure multiple certified copies of your divorce decree and settlement agreement. Financial institutions, government agencies, and creditors often require official copies before making changes .

Pro tip: Order at least 5-10 certified copies—you'll be surprised how many places need them.

Name Change Process If Applicable

If you're returning to a former name, start with the Social Security Administration (SSA). You'll need your certified divorce decree and birth certificate . After updating your Social Security card, visit the DMV for a new driver's license, then update your passport .

Government Agencies

Notify the IRS, voter registration office, and any professional licensing boards of your name or address change . Don't rely on mail forwarding—it's not reliable for official documents .

Create a Master File

Organize all your post-divorce documents in one place: decree, settlement agreement, updated IDs, property deeds, QDROs, and financial account information . This saves time and reduces stress when updates become time-sensitive.

Social Security Name Change Requirements

Apply in person at your local SSA office. Processing takes 10-14 days .

Step 2: Retirement Accounts – The Most Overlooked Step

The QDRO Requirement

Qualified Domestic Relations Order (QDRO): A specific legal document required by the plan administrator to divide 401(k)s, pensions, and other retirement accounts without triggering tax penalties or early withdrawal fees .

Timeline: QDROs can take 3-6 months to draft, submit, and get approved by the plan administrator. Start immediately .

401(k)s and Pensions

Work with your attorney or a QDRO specialist to draft and submit the QDRO to the plan administrator. Track its progress and confirm the funds have been transferred.

IRAs (No QDRO Required)

IRAs don't require QDROs, but you must follow IRS transfer rules. Work with your financial institution to complete the transfer under the "divorce transfer" provisions to avoid taxes.

Update Beneficiaries

Remove your ex-spouse as beneficiary on all retirement accounts—unless your decree specifically requires otherwise . This is often overlooked but critically important.

Step 3: Real Estate, Vehicles, and Property Transfers

Removes one spouse's name from property title

Ensures property passes to intended beneficiaries

DMV requires updated title and registration

Register with appropriate state agency

Real Estate Transfers

If the decree awarded your spouse the house, you need to sign a quitclaim deed to remove your name from the title. But this does not remove you from the mortgage .

Critical: The spouse keeping the house must refinance to remove the other spouse's liability. Until then, both remain responsible to the lender .

Mortgage Refinancing

If ordered in the decree, ensure refinancing is completed promptly. Track deadlines—failure to refinance can keep you tied to your ex's financial decisions for years.

Vehicle Titles

Visit the DMV with your certified decree to transfer vehicle titles. If there's a loan, the spouse keeping the car must refinance .

Utility and Service Transfers

Transfer electricity, gas, water, trash, internet, and streaming services into the appropriate spouse's name . This protects credit scores and ensures service continuity.

The Refinancing Trap

"Even if a court assigns responsibility to one party, lenders still view both names on the loan as equally responsible until it is refinanced or paid off" . If your ex stops paying, your credit suffers—and you may be forced to pay to avoid foreclosure.

Step 4: Bank Accounts, Credit Cards, and Liabilities

Close Joint Accounts

"Close or separate all joint checking, savings, and credit card accounts" . Leaving your name on an account makes you responsible for future charges made by your former spouse .

Open New Individual Accounts

Open new bank accounts and credit cards in your name only. Update direct deposits and automatic payments .

Remove Authorized Users

Remove your ex-spouse as an authorized user on your individual credit cards, and ensure they remove you from theirs .

Refinance Debts

For mortgages, car loans, and personal loans, refinance into individual names as specified in the decree .

Monitor Credit Reports

Request free credit reports from Equifax, Experian, and TransUnion. "Review them carefully for joint debts, unauthorized accounts, or missed payments, and dispute any inaccuracies immediately" .

Equifax

annualcreditreport.comExperian

annualcreditreport.comTransUnion

annualcreditreport.comStep 5: Insurance – The Overlooked Financial Risk

Health Insurance

Life Insurance

Homeowner's Insurance

Auto Insurance

Health Insurance 60-Day Window

If you lost coverage through your spouse's plan, divorce qualifies you for a Special Enrollment Period . You typically have 60 days to enroll in new coverage.

Life Insurance Beneficiaries

Review and update beneficiaries on all life insurance policies. If your divorce requires you to maintain coverage for child support or alimony, ensure the policy designations match the decree .

Set reminders: If your ex must maintain coverage, follow up annually to verify premiums are paid .

Home and Auto Insurance

Update policies to reflect new ownership and remove your ex-spouse from coverage where appropriate . Update your address and any additional drivers.

Step 6: Estate Planning – Don't Let Your Ex Inherit Everything

Shocking fact: If you don't update your will and beneficiary designations, your ex-spouse could still inherit your assets—even if your divorce decree says otherwise . Beneficiary designations on retirement accounts and insurance policies generally override what's in your will .

Create a New Will

In many states, divorce invalidates provisions that benefit your ex-spouse, but relying on default state rules can lead to unintended outcomes . Create a new will that reflects your current wishes.

Update Powers of Attorney

If your ex-spouse is named as your financial or medical power of attorney, immediately designate someone else to make decisions on your behalf if you become incapacitated .

Health Care Proxy

Name someone you trust to handle medical decisions. This is separate from your financial power of attorney .

Revise Trusts

If you have trusts supporting children or managing assets, ensure they align with your post-divorce goals .

Step 7: Children – Practical and Legal Updates

Notify Schools and Care Providers

"Contact your children's schools and care providers to inform them of your updated custody arrangements. Provide a certified copy of the final divorce decree to the school, so they have accurate information on file" .

Review Custody Agreements

Ensure you fully understand the custody schedule and obligations. Clarify any confusion with your attorney to avoid future conflicts .

Update Emergency Contacts

Update emergency contact forms at schools, doctors, and activities.

Co-Parenting Communication

"If you attempt to begin your co-parenting relationship with your ex-spouse in the same way you ended your marriage, you will be in some trouble" .

- Establish preferred communication methods early

- Keep conversations businesslike and child-focused

- Use co-parenting apps if direct communication is difficult

- Don't let personal animosity drift into co-parenting

- Consider counseling if children are struggling

Step 8: Tax Status and Filing Considerations

Determine New Filing Status

Your filing status is generally "single" for the entire year if you're divorced by December 31. Head of household may be available if you have a dependent child and meet IRS criteria .

Claiming Dependents

Verify who is entitled to claim the children based on your decree. This may alternate years or be allocated entirely to one parent .

Update Withholding

Submit a new W-4 to your employer to ensure correct tax withholding based on your new filing status .

Child Tax Credit

Understand how the child tax credit applies to your situation .

In England and Wales, the divorce decree itself does not dismiss financial claims. A separate Financial Order is required to make the settlement legally binding and enforceable. Without it, claims can be pursued years later .

Step 9: Create Your Post-Divorce Financial Plan

Build Two Budgets

Create one budget for negotiations (if still open) and one for real life. Understand your new income, expenses, and savings capacity .

Rebuild Emergency Fund

Divorce often depletes savings. Prioritize rebuilding your emergency fund .

Revisit Retirement Planning

With your new financial picture, update your retirement plan with a financial advisor .

Monitor Your Credit

Set up credit monitoring to catch any issues early .

"Debt is the number one reason why people cannot avail themselves well. When you have debt in your life, it prevents you from improving your circumstances financially and saving for your future" .

Step 10: Personal Well-Being and Goal Setting

Assess Your Support Network

Expand your support network if you're on your own or have children . Connect with friends, family, or support groups.

Set Concrete Goals

"A goal needs to be your own, it needs to be concrete, and it needs to be in writing" . Focus on personal, financial, and relational goals.

Stay Healthy

Prioritize physical and mental health. Divorce is stressful—take time for self-care .

Celebrate Progress

Acknowledge the work you've done. Each completed task brings you closer to stability and independence.

Implementation Is Everything

The divorce decree is not the finish line—it's a blueprint that requires you to do the construction work . Nothing happens automatically. Every bank account, every insurance policy, every retirement plan, every piece of real estate needs your active attention.

Create a master checklist and work through it methodically. If you feel overwhelmed, enlist help: your divorce attorney can assist with QDROs and property transfers; a financial advisor can help with budgeting and retirement planning; a therapist can support your emotional transition .

Completing these post-divorce tasks may not feel as satisfying as walking out of the courthouse with your decree in hand. But months and years from now, when your accounts are clean, your credit is strong, your estate plan reflects your wishes, and your children are thriving, you'll know that the real work after divorce was what secured your fresh start.